Bilt Rewards banks $60M development on a $350M evaluation to advance credit card benefits for renters

The latest round comes just 90 days from Bilt’s launch….

The latest round comes just 90 days from Bilt’s launch….

Six-year-old Bangalore-based fintech Razorpay, which was valued at $3 billion in a financing round in April this year, has actually courted one more high-profile investor: Salesforce Ventures. Razorpay stated on Monday it has received a “tactical financial investment” from the venture arm of the American enterprise giant. The investment will help the startup “additional enhance its existence […] Razorpay stated on Monday it has gotten a “tactical financial investment” from the endeavor arm of the American business giant.”At Razorpay, we want to make additional strides on the idea of investing in India’s digital future and developing a smart payment and banking infrastructure for the new-world. Monday’s offer is Salesforce Ventures’ 2nd financial investment in the Indian start-up community. …

Ascend is moving insurance coverage into the digital age by with a payments platform that integrates financing, collections and payables….

Structure credit rating can be hard if you are

a customer that is having problem getting access to credit in the very first location. Get in TomoCredit, which has actually established a charge card focused on developing credit rating for first-time customers. The San Francisco-based startup is revealing today that it has actually raised $10 million in a Series […]

, which has developed a credit card focused on constructing credit history for novice debtors. TomoCredit co-founder and CEO Kristy Kim came up with the concept for the company business being rejected multiple numerous for an auto vehicle while in her early 20s. The fintech offers a credit card intended at helping novice debtors develop credit history, based on their money circulation, rather than on their FICO or credit report rankings. The start-up prepares to use its new capital to do more hiring and improve functions such as weekly autopay and high credit limits in an effort to”enhance credit scores quicker,”she included. Enter TomoCredit, which has developed a credit card focused on constructing credit history for novice borrowers….

There’s a new entrant in Southeast Asia’s growing list of unicorns. Jakarta-based Xendit, best understood for its digital payment facilities however also focused on other monetary items, announced today it has actually raised $150 million in Series C funding, bumping its evaluation to $1 billion. The round was led by Tiger Global Management, with participation from […] Xendit chose to raise once again since to sustain growth into other nations, Wijaya told TechCrunch. Xendit’s edge is combining a global method with its extreme focus on localization, Wijaya stated. In a press statement, Tiger Global Management partner Alex Cook stated, “Xendit’s digital payments facilities, constructed particularly for Southeast Asia, is quickly ending up being the standard for financial operations in the region. …

SellersFunding produced a financing and financial services platform to enhance global commerce for thousands of markets, including working capital, cross-border cash management and taxes. He established the company in 2017, and today has actually over 30,000 signed up users and is approaching $10 billion in sales volume that is feeding information into SellersFunding’s everyday models. SellersFunding has actually consistently grown 300% year over year, Pero stated. “Normal banks like Barclay can’t check credit. SellersFinding is assisting small services get this credit, and rightly so. …

Last year at this time, SpotOn was on the edge of revealing a $60 million Series C funding round at a $625 million valuation. Quick forward to nearly precisely one year later on, and a lot has altered for the payments and software application startup. Today, SpotOn stated it has closed on $300 million in Series E […] Given that its 2017 creation, SpotOn has actually been focused on supplying software and payments innovation to SMBs with an emphasis on dining establishments and retail organizations. The acquisition of Appetize extends SpotOn’s reach to the enterprise area in a significant method. SpotOn is taking on the likes of Square in the payments space. SpotOn will now have over 500 employees on its item and technology team, according to co-founder and co-CEO Zach Hyman. …

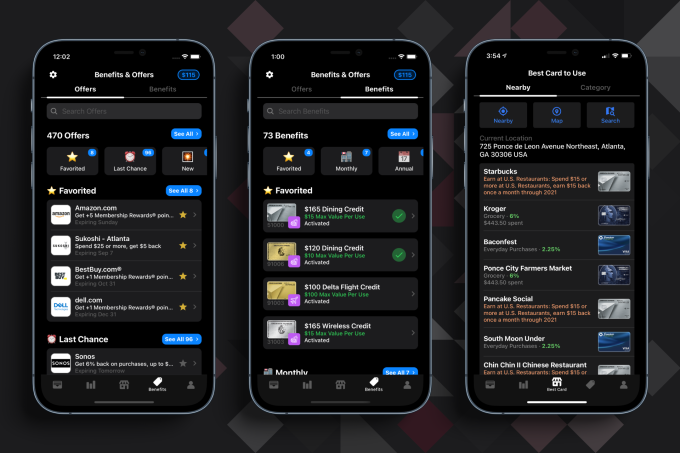

MaxRewards is a digital wallet app that manages credit cards and instantly triggers advantages like rewards, cashback offers and regular monthly credits. , a digital wallet app that manages credit cards and automatically triggers advantages like benefits, cashback offers and monthly credits. Tracking his own credit cards manually prior to MaxRewards, Khan remembered in one year, getting $16,000 in benefits. Utilizing those benefits was hard and time-consuming, because the cost savings and benefits aren’t constantly made apparent by the credit card companies. MaxRewards offers deals benefitsAdvantages …

Scalapay, a buy now, pay later (BNPL) technology provider that has made significant headway with retailers and consumers in Europe and in categories like fashion, has closed a round of funding that it will be using to fuel its expansion ambitions. The startup has raised $155 million at a $700 million valuation. Tiger Global is […] …

Gig and independent workers have different needs when it pertains to monetary products than salaried workers at a business. It’s an obstacle that Tilak Joshi, creator of Lean, ended up being acutely knowledgeable about throughout his tenure as head of Mint and years as an item exec at American Express and PayPal. While the U.S. has actually seen […] Upon leaving Mint in 2020, Joshi founded Lean to support gig workers with a platform that offers access to financial products that he states are “custom-made built” for their needs. Lean aims to assist independent workers by partnering directly with markets to offer financial items and benefits. Lean works with markets of all sizes that employ either 1099 or W2 employees that work in industries such as ride-hailing, building and construction, courier and health care.”There are substantial market tailwinds to better serving gig employees, and markets are significantly searching for better ways to bring in and maintain their workers,” he composed via e-mail. — TechCrunch” src=”https://techcrunch.com/2021/05/06/how-much-product-room-will-fintech-giants-leave-for-startups/embed/#?secret=77hkQbAvrO” data-secret=”77hkQbAvrO” width=”800″ height=”450″ frameborder=”0″ marginwidth=”0″ marginheight=”0″ scrolling=”no” > …

Recent Comments