Lemonade, a heavily-backed start-up that offers occupants and property owners insurance coverage to consumers, submitted to go public today. Thecompany( backed by SoftBank, part of the Sequoia empire, General Catalyst and Tusk Endeavor Partners, to name a few )releasing its financial outcomes helps shed light on the burgeoning insurtech market, which has actually drawn in an ocean of capital in recent quarters. TechCrunch covered a part of the insurtech world earlier this year, asking why insurance marketplaces were picking up so much investment, so quickly. Lemonade is various from insurance coverage marketplaces because it’s a full-service insurance supplier.

As its S-1 notes:

By leveraging technology, data, information intelligence, contemporary designModern style behavioral economics, we believe we are making insurance more delightful, more affordable, budget friendly precise, exact more socially impactful. To that end, we have developed a vertically-integrated business with wholly-owned insurance providers in the United States and Europe, and the full innovation stack to power them.

Looking at the numbers, the pitch is a bit forward-looking.

Parsing Lemonade’s IPO filing, business reveals that while it can produce some margin from insurance coverage, it is still miles from having the ability to pay for its own operation. The filing advises us more of

Vroom’s similarly unprofitable offering than Zoom’s remarkably profitable debut. The numbers Lemonade is targeting a$100 million IPO according to its filings. That number is imprecise, however directionally beneficial. What the placeholder target informs us is that the business is most likely to attempt to raise $100 million to $300 million in its launching than it is to take objective at $500 million or more.

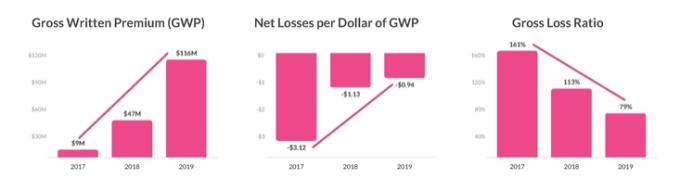

First, this trio of bar charts that are up leading in the filing:

Gross composed premiums(GWP )is the total quantity of profits expected by Lemonade for its offered insurance items, significantly discounting commissions and some other costs. As you ‘d anticipate, the numbers are going up in time, implying that Lemonade was effective in offering more insurance products as it

aged. The 2nd chart information just how much cash the company is losing on a net basis compared to the company’s gross written premium result. This is a faff metric, and one that isn’t too motivating; Lemonade’s GWP more than doubled from 2018 to 2019, however the firm’s bottom lines per dollar of GWP fell far less. This indicates less-than-stellar operating take advantage of.

The last chart is more encouraging. In 2017 the business was paying even more in claims than it took in from premiums. By 2019 it was producing margin from its insurance items. The trend line here is likewise nice, in that the 2018 to 2019 enhancement was steep.

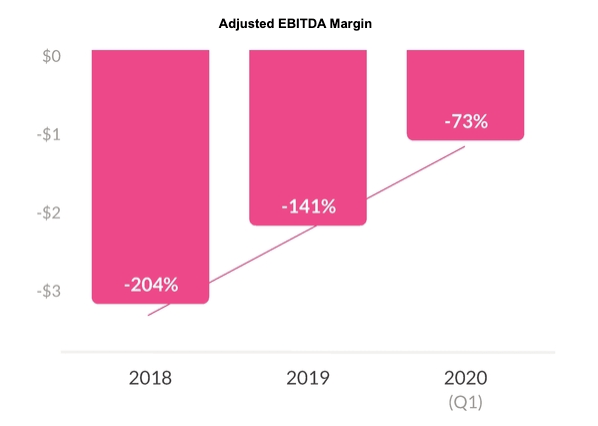

And then there’s this one:

This looks great. That said, improving changed EBITDA margins that remain starkly unfavorable as something to be proud of is really Unicorn Age. 2020 is alive with animal spirits, so perhaps this will engender some public financier adulation.

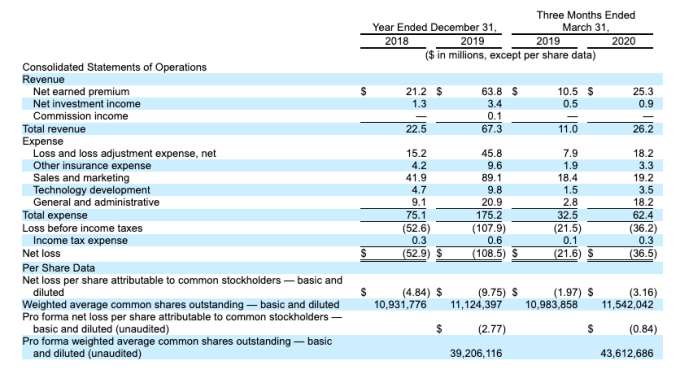

Regardless, let’s go into the numbers. Here’s the primary income declaration:

Some definitions. What is net made premium? According to the company it is “the made part of our gross written premium, less the made portion that is ceded to third-party reinsurers under our reinsurance contracts. “Like pre-sold software application earnings, premium earnings is “earned professional rata over the regard to the policy, which is typically.” Cool.

Net investment earnings is “interest earned from repaired maturity securities, short-term securities and other financial investments.” Cool.

The 2 numbers are the business’s only material income sources. And they sum to great deals of growth. From $22.5 million in 2018 to $67.3 million in 2019, a gain of 199.1%. More recently, the business’s Q1 results saw its revenue grow from $11.0 million in 2019 to $26.2 million in 2020, a gain of 138.2%. A slower speed, yes, but from a higher base and more than large adequate for the company to show off growth to a yield-starved public market.

Now, let’s talk losses.

Deficits

We’ll talk margins a little later, as that bit is frustrating. What matters is that Lemonade’s cost structure is suffocating when compared to its ability to pay for it. Net losses increased from $52.9 million in 2018 to $108.5 million in 2019. More just recently, a Q1 2019 bottom line of $21.6 million was smashed in the first quarter of 2020 when the company lost $36.5 million.

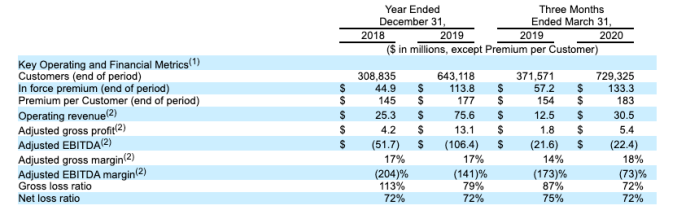

Lemonade only appears to lose more cash as time goes along. So how is the company turning a lot growth into such huge losses? Here’s a hint:

This is unpleasant, however we can get through it. Initially, see how operating earnings is different than the GAAP revenue metrics we saw previously? That’s because it’s a non-GAAP(adjusted )number that suggests the “overall income prior to adding net investment earnings and before subtracting earned premium ceded to reinsurers.” Cool.

That interest aside, what we really appreciate is the company’s adjusted gross earnings. This metric, defined as “total earnings excluding net financial investment earnings and less other costs of sales, including bottom line and loss adjustment expenditure, the amortization of deferred acquisition expenses and charge card processing costs,” which indicates gross profit however incredibly not actually, is irksome. Given that Lemonade is already changing it, it’s significant that the business just managed to generate $5.4 countless the stuff in Q1.

Remember that the company had GAAP profits of $26.2 million because three-month period. So, if we adjust the firm’s gross earnings, the business end up with a gross margin of just a hair over 20%.

What? The company is spending greatly– $19.2 million in Q1 alone– on sales and marketing to create relatively low-margin earnings. Or more specifically, Lemonade produced enough adjusted gross profit in Q1 2020 to cover 28% of its GAAP sales and marketing invest for the exact same duration. Figure that one out.

Anyway, the company raised $300 million from SoftBank in 2015, so it has lots of money. “$ 304.0 million in money and short-term investments,” as of the end of Q1 2020. So, the business can sustain its Q1 2020 operating cash burn ($19.4 million) for a very long time. Why go public then?

Article curated by RJ Shara from Source. RJ Shara is a Bay Area Radio Host (Radio Jockey) who talks about the startup ecosystem – entrepreneurs, investments, policies and more on her show The Silicon Dreams. The show streams on Radio Zindagi 1170AM on Mondays from 3.30 PM to 4 PM.

Recent Comments